How To Place The Perfect Stop Loss (I Ran 480,000 Simulations)

Every trader hunts for the perfect stop loss. The perfect distance, the perfect type, the magic setting that finally stops the market from taking them out. So I ran 480,000 simulations on 15 years of price action to settle it. The answer is not a magic number. It is two decisions, and most people get both wrong.

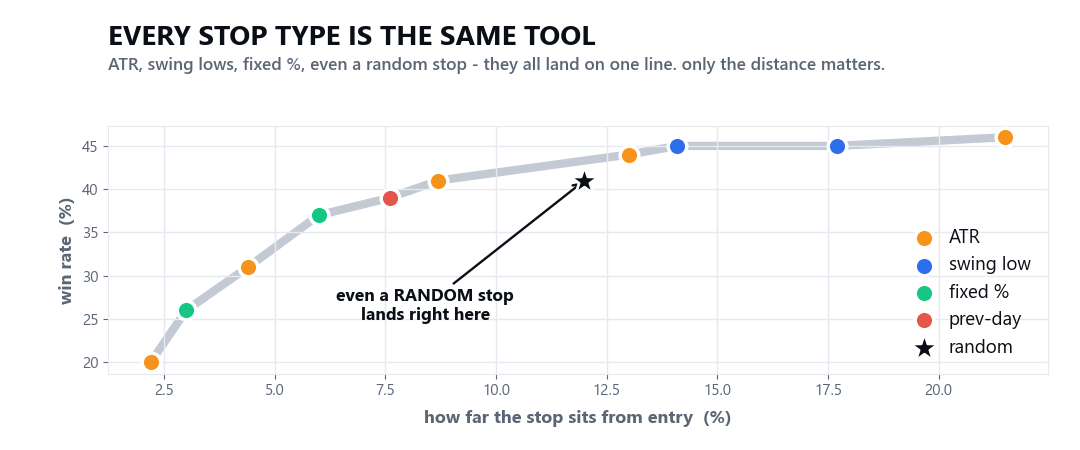

Myth 1: the stop type does not matter

ATR versus swing lows versus a fixed percent is the fight everyone has. Traders will argue about it for hours. So I plotted every type from 480,000 runs onto one chart, and they land on the exact same line.

At the same distance from your entry, an ATR stop, a swing low and a fixed percent all won the same, lost the same, made the same. I even ran a control, a stop placed at a random distance every single trade, and it landed right on the line too. The type is a myth. It is just a different way to set the one thing that matters, the distance.

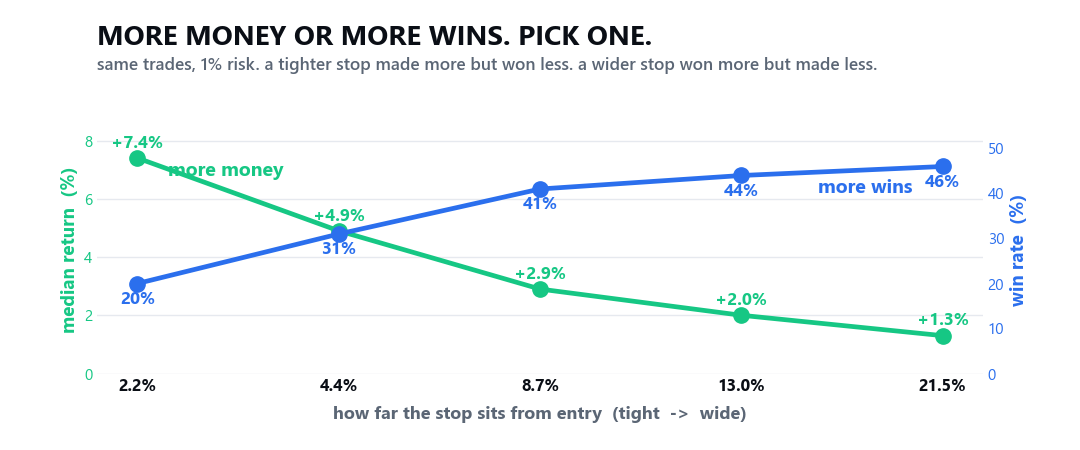

The real dial: how far you place it

The distance is where it gets interesting, because it does not decide whether you make money. It decides how.

Place the stop tight, about 2 percent away, and you made the most, plus 7.4 percent, but you won only 20 percent of the time and got chopped out of 79 percent of your trades. Place it wide, about 21 percent away, and you won 46 percent of the time but made the least, plus 1.3 percent. More money or more wins. You get one, never both. There is no perfect distance, only the one that fits how you trade.

The tight-stop trap

That result whispers go tight, it pays more. Do not listen. The tight-stop edge is a 20 percent win rate propped up by a few lucky monster trades, and the simulations do not even charge the slippage you eat getting stopped out four times out of five. In the real world that slippage bleeds the edge away. And almost nobody can lose eight trades in a row and keep clicking buy. A tight stop is a sniper's game most people quit right before it pays. Pick the win rate you can actually hold.

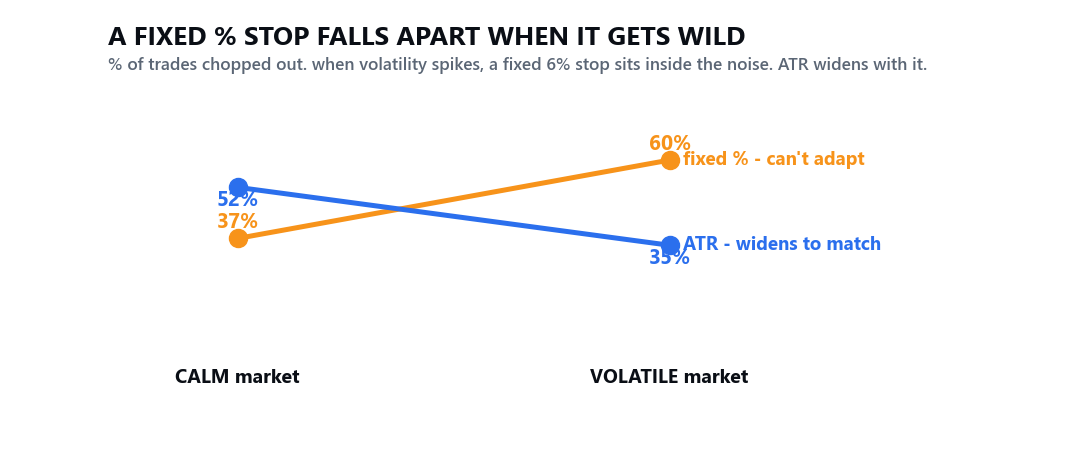

Why I still use ATR

If the type is equal on average, why recommend one at all? Because one of them adapts. Watch what happens when the market turns volatile.

When volatility spikes, a fixed 6 percent stop suddenly sits inside the noise. It gets chopped out 60 percent of the time and its win rate drops to 33 percent. It cannot tell the market changed. An ATR stop widens automatically to match, so it stays composed, chopped just 35 percent, exactly when the fixed stop falls apart. ATR does the adjusting for you. A fixed number cannot.

How to place the perfect stop

Put it together into four steps you can run on every trade.

- Measure the noise with ATR. The ATR is the average size of a normal move, plotted in one click on most platforms.

- Place the stop beyond the noise. Set it 2 to 3 times the ATR from your entry, so a normal wiggle cannot tag it. Never a tight round number.

- Pick your win rate. Wider means you win more often and sleep better. Tighter means you win rarely but big. Choose the one you can hold through a drawdown.

- Size the trade to the stop so a stop-out costs the same small slice of your account every time. This is the piece that quietly matters most, and it is where this series is headed.

ATR for the type. Your win rate for the distance. The perfect stop was never a setting you could copy. It is a process you repeat.

I break down the market like this every day, free, on Instagram. To trade alongside me and the community, come to bitcoindaily.vip.

Educational, not financial advice. Every cycle is different and past performance is not a guarantee.

We break down the market like this every day, free on Instagram and YouTube, and in depth inside the community.

Education, not financial advice. Trading involves real risk.